Q1 2021: Freight Market Update

Explore Q1 2021 freight market update based on Vortexa data.

At the end of last year we sought to identify the main trends that will shape the 2021 freight markets. Firstly we urged market participants to follow floating storage as the main balancing factor for freight markets with persistent oversupply carried into the new year. Furthermore, we decided to keep an eye out on Chinese imports of crude oil as the main contributor to tanker tonne-miles in this market segment. When it comes to clean petroleum products (CPP) markets we were hopeful this would be the tanker market bright spot as refinery outages and closures would spur volumes of oil-on-water, boosting tonne-miles and utilisation.

Looking ahead, we expect the recent announcement of OPEC+ producers to boost output from May onwards, in line with seasonal demand peaks to spur tonne-miles within crude tanker markets whilst continued rollouts of vaccines across the world help ease national lockdowns. However, economic recovery will be uneven across regions.

-

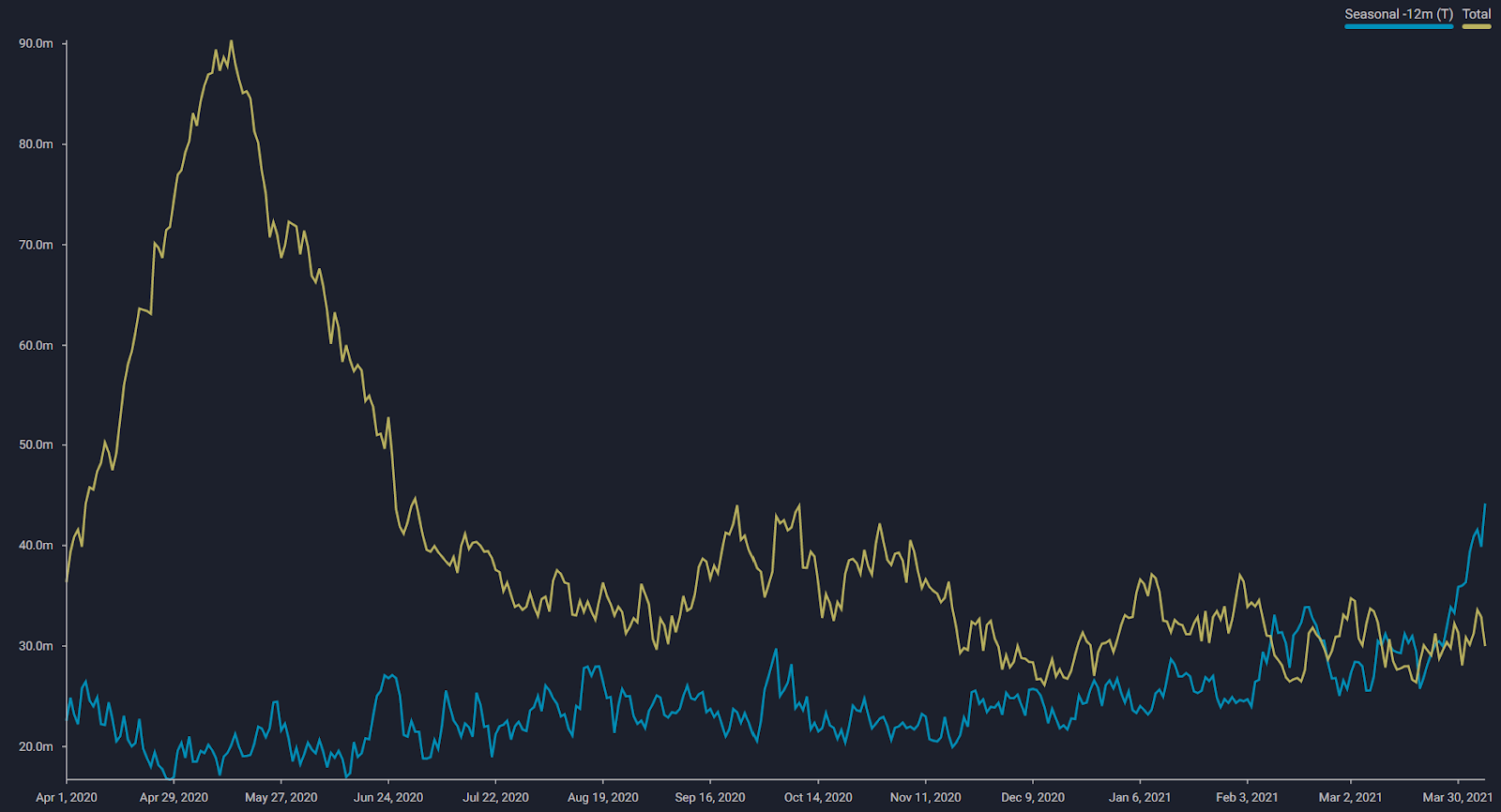

CPP floating storage destocking indicates strength in demand

- Last 2 years of Diesel/Gasoil & Gasoline global floating storage (see this in the platform)

-

- As predicted, the unravelling of the floating storage left its impact on the freight market so far in 2021, especially for VLCCs. Global crude and fuel oil floating storage on VLCCs remained flat around pre-pandemic levels, triggering an oversupply that has subsequently weighed on VLCC freight rates as tonnage availability rose in Q1, according to Vortexa data.

- Similarly, the destocking of CPP floating storage resumed throughout 2021 on the back of strengthening diesel and gasoline prices across the board. More specifically, diesel/gasoil and gasoline floating storage ended Q1 2021 below 1-year ago levels

- Going forward, OPEC+ production and thus OPEC+ exports are expected to support dirty freight rates. At the same time, the role of floating storage in the freight market is poised to become less significant, as market conditions are not conducive with volumes brought back to pre-pandemic levels. Nevertheless, an unsustainable rise in diesel exports could propel a rebound in CPP floating storage. Evidently, the short-term contango for gasoil is strengthening since mid-February, according to Argus Media.

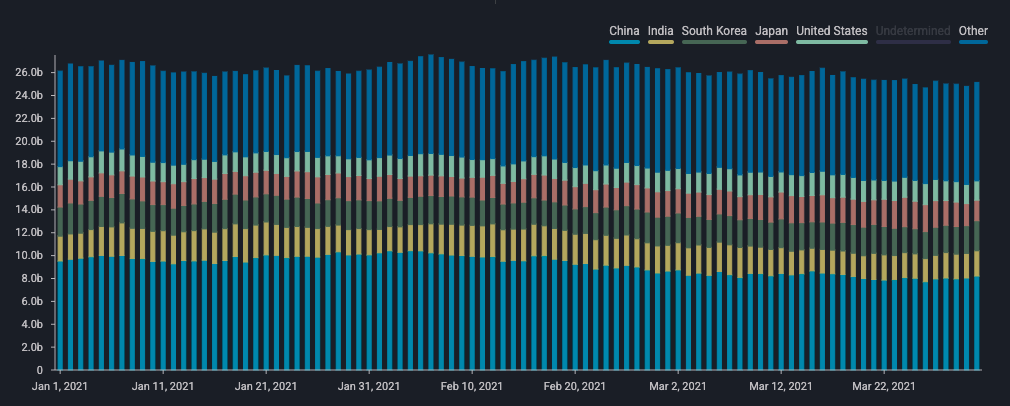

Chinese imports keep crude tonne-miles alive

Crude tonne-miles in Q1 2021 by destination (see this in the platform)

- We predicted China’s appetite for crude will remain the most important driving force in 2021 on which the fortunes of the shipping market will be largely dependent. As of the end of Q1, this has largely been the case with China remaining the top contributing destination to tonne-miles for the crude tanker market according to our data.

- Vortexa data shows that Chinese imports contributed 830 bn or 35% of crude tonne-miles for Q1. The volume of Chinese crude imports highlights the outsized reliance of the crude tanker markets on one buyer.

- An interesting point to note concerns tonne-miles contributed by Indian imports. They witnessed a drop of 25% from a quarter-high in January 2021 as resurging coronavirus cases in the country have hampered economic recovery. However, its desire to address its dependency on Middle Eastern, in particular Saudi, crude imports will lead it to purchase crude from further abroad. India may well see the highest increase in percentage terms in tonne-miles during Q2.

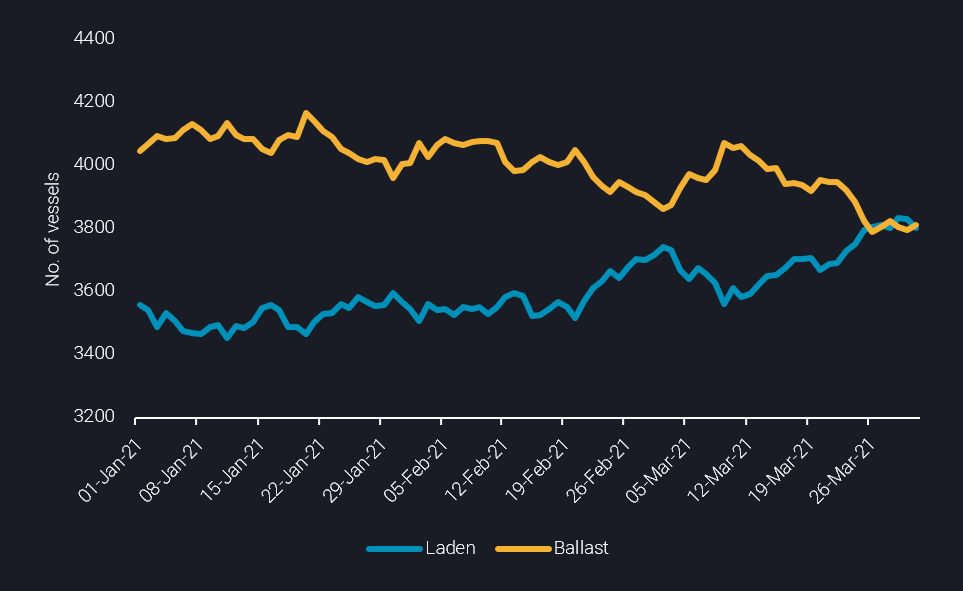

Recent developments lift CPP tanker utilisation

CPP tanker utilisation in Q1 2021 (see this in the platform)

- It is not a secret that clean tankers have performed considerably better than the last quarter, as earnings improved throughout Q1 2021.

- Several developments that shook the freight world in the first quarter of the year, ended up benefiting the CPP tanker classes. Just to name a few:

– Australia’s decision to shut down refineries boosting CPP tanker tonne-mile demand towards the region.

– The Texas cold snap that was followed by a decline in US refinery runs increasing transatlantic flows ex-Europe.

– The higher olefin margins for steam crackers in Asia, which boosted naphtha demand from Europe and Asia.

– The current improvement in gasoline cracks as we move to summer-grade material and the seasonal demand peak, boosting MR and Handysize tanker utilisation. - This is also reflected when looking at the bigger picture of the CPP tanker fleet. The number of laden CPP tankers have followed a rising pattern since the start of the year. By the end of Q1 utilisation managed to edge over 50%, as the number of laden CPP tankers surpassed the ballast ones.

- An easing of European pandemic lockdown measures and a prospective increase in jet fuel flows as transportation demand bounces back, will continue to support the utilisation of CPP tankers.

Review the quarter in Freight – Vortexa Analysis

Q1 2021 Vortexa Special Reports/Infographics feat. Freight

- March: Infographic: Cargoes stuck in Suez

- March: Report: The changing landscape of fuel oil trade flows

- March: Infographic: The freeze on Texas refined product exports

- January: Report: Opportunities in crude freight and storage markets

Q1 2021 Vortexa Blogs feat. Freight

- March 19: Middle East LR2 tankers: Naphtha provides a lifeline

- March 11: US gasoline demand moulds the Atlantic MR market

- March 4: Johan Sverdrup: Contradicting Fates for Crude Tanker Classes

- February 25: Identifying trading opportunities through oil tanker shipping routes

- February 23: Altona’s refinery closure: implications on trade flows and freight

- February 17: Snapshot: Europe to PADD 1 diesel flows remain buoyant

- January 20: LNG freight rates follow surge in exports

- January 7: More CPC Blend to sail to Asia in Q1 2021

Want to know more about our leading freight indicators?

{{cta(‘bed45aa2-0068-4057-933e-3fac48417da3’)}}