FT Commodities Global Summit 2025: Vortexa joins as Gold Sponsor

We were proud to return as Gold Sponsors to the 2025 FT Commodities Global Summit in Lausanne. As we gather reflections on the event discussions, we share our latest observations in global oil.

Over the course of three days, we witnessed multiple conversations about the difficulties in securing a stable market amid persistent geopolitical challenges, driven to some extent by the pace and scope of the US President’s executive orders. In light of these themes, I had the pleasure of joining a speaker panel “Oil – Are prices stabilising to a new normal?” alongside industry experts from Trafigura, Gunvor, SOCAR Trading, RBC Markets, and Financial Times.

We have previously shared our take on whether global uncertainty implies market volatility, concluding that volatility has ultimately manifested in the freight markets, whereas oil prices have remained range-bound amid muted growth in global supply and demand for the past two years.

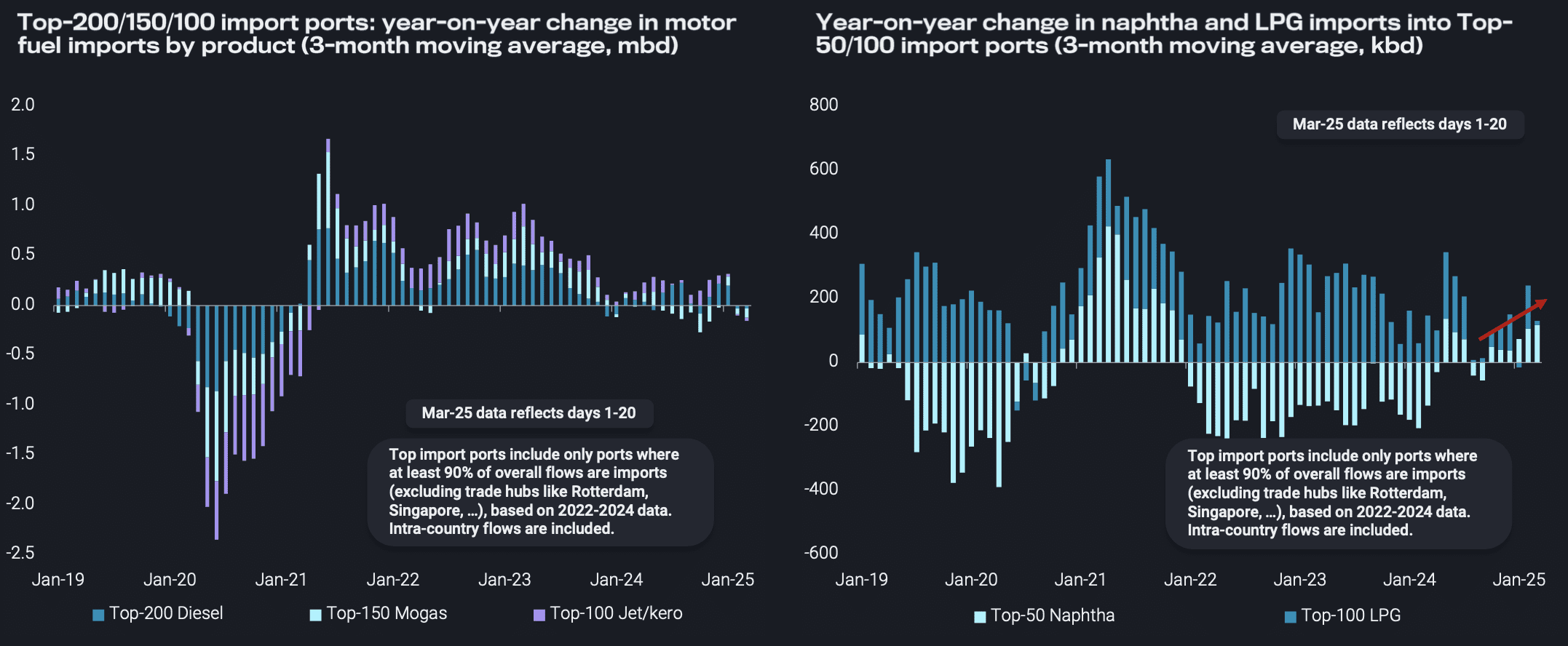

The oil products side has not signalled much hope for demand in early 2025, a notion also shared by other speakers and participants at the conference. Vortexa data indicates motor fuel demand has come to a standstill since December, making spare global refining capacity an issue with shutdowns scheduled all over the globe. Only naphtha is doing a bit better, as LPG export availability from the US is hitting temporary capacity restrictions (right-hand side chart below).

LHS: Mogas 100 &101-150, Diesel 100 & 101-200, Jet 100. RHS: Top-50 naphtha, Top-100 LPG

Perhaps the most outstanding feature of oil markets early in 2025 is a huge rerouting of crude away from the Atlantic Basin to the Pacific Basin, driven by Asian buyers being concerned about future supplies from Iran and Russia. We have seen 1.7mbd less crude being directed to the Atlantic Basin in Q1 2025 than a year earlier. Instead, these barrels are targeting eastern markets with a notable swing of more than 500kbd of CPC Blend and North Sea grades towards Asia over February and March.

One of the most frequently asked questions is whether Iran can evade a maximum pressure policy from the US. This question will ultimately be decided in Beijing, and we tend to think that China is unwilling to let the US dictate its third-party trading relationships. We have noticed regular adjustments to logistical approaches, including more STS activity, but also the discharge by sanctioned tankers. Chinese policy makers may see the independent (also from global finances) teapot sector as a virtue rather than a vice in this context.

Much doubt has been uttered on how the above and general market workings are to be squared with the placed target of $50/b oil prices. We would also tend to argue that the US is pretty alone with such an objective, as oil producers (inside and outside OPEC+) surely want higher prices, and also consuming nations like China and the EU may not facilitate lower prices given their energy transition agendas, which work better with higher oil prices.

Of course, oil prices could go lower if OPEC+ brings barrels back, demand continues to disappoint, and more supply – especially in the Americas – comes onstream. But will all this really happen at the same time? OPEC+ has shown a very solid grip on market fundamentals, and we expect this approach to prevail. In spite of all this uncertainty, most players agree that the most likely outcome for oil prices is more of the same – somewhere around $65-75 per barrel on an average basis.