China and India crude slate pivots post sanctions

China and India have quickly responded to widespread sanctions applied to tankers carrying Russian crude oil, as seen in recent changes to trade activity. In this insight, we explore the common and differing approaches taken by these two key crude importers to mitigate short-term supply disruptions.

Vortexa flows data shows shifts in exports flows targeting India and China from the major crude producing regions since 10 January – when the US Office of Foreign Assets Control (OFAC) applied its largest batch of sanctions on over 100 tankers involved in Russian oil trade.

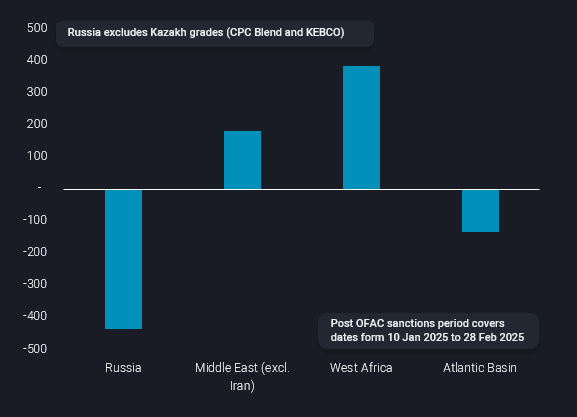

Since 10 January, Russian crude exports to India and China (combined) have slowed, even considering seasonal patterns. Meanwhile exports from West Africa and the Middle East have picked up, but other Atlantic Basin producers show no signs of rising exports to India/China, at least for now (see chart below).

Crude exports to China and India post OFAC sanctions vs 2024 average, split by origin region (kbd) (flows link)

A comparison of Russian-origin crude exports post 10 January sanctions, versus average export volumes across 2024, shows a decline of around 450kbd. In comparison, Middle East (excluding Iran) exports are up by 200kbd, but the most significant change is West Africa, up sharply in recent weeks by about twice as much as Middle Eastern flows. The strong uptick in West Africa exports is also motivated by wide Brent-Dubai spreads, which make West African crudes (priced against Brent) relatively cheap in comparison to Middle East grades.

Within West Africa, a closer look reveals that the main driver of this increase are rising exports from Angola to China. Post-sanctions exports (10-Jan to 28-Feb) have crossed the 700kbd mark and in turn have restricted exports to Atlantic Basin buyers (Spain, Netherlands, Italy and Brazil).

Unlike China, India is not a major historical buyer of Angolan crude but exports to India are up m-o-m in February, along with those from Republic of Congo and Cameroon.

Outside of West Africa, the only other region showing in increase in exports to China/India is the Middle East. With more than half of the tanker fleet that was recently carrying Russian-origin crude now under OFAC sanctions, it makes sense for buyers to look to a region containing multiple ports with large VLCC loading capacity and close proximity to Asia, particularly India.

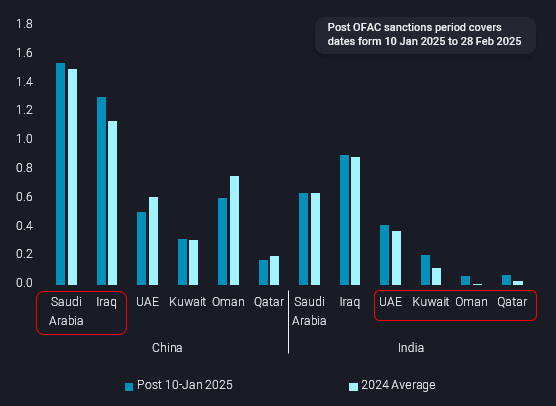

Selected Middle East countries’ crude exports to India and China, post-Jan sanctions vs 2024 average (mbd)

Looking at the changes in exports after January 2025 sanctions, we see China’s historically larger Middle East suppliers (Saudi Arabia and Iraq) have increased exports the most, at the expense of other producers. In contrast, India has taken on incrementally more from relatively smaller suppliers (UAE, Kuwait, Oman and Qatar), while keeping exports from Saudi Arabia and Iraq flat.

When viewed in conjunction with the trends seen with West Africa exports, it seems at least from an initial perspective, OFAC sanctions in January have driven India to diversify crude supply while China is becoming more consolidated around its historically large suppliers. This also fits with the sharp response by China (fresh STS activity, reported port group ownership changes) to maintain Russian Far East ESPO flows into China as much as possible.

Looking ahead, the potential divergence in crude procurement by India and China will be overlaid by OPEC+ beginning its delayed return of barrels into the market from April. With Saudi Arabia and the UAE likely to be the biggest contributors to this, we could see another pivot, particularly in India’s case, towards the largest producers again.