Europe’s crude slate sweetens after the loss of Urals

This insight explores Europe’s crude/condensate imports, its replacement of Russian Urals and the implications for its crude slate.

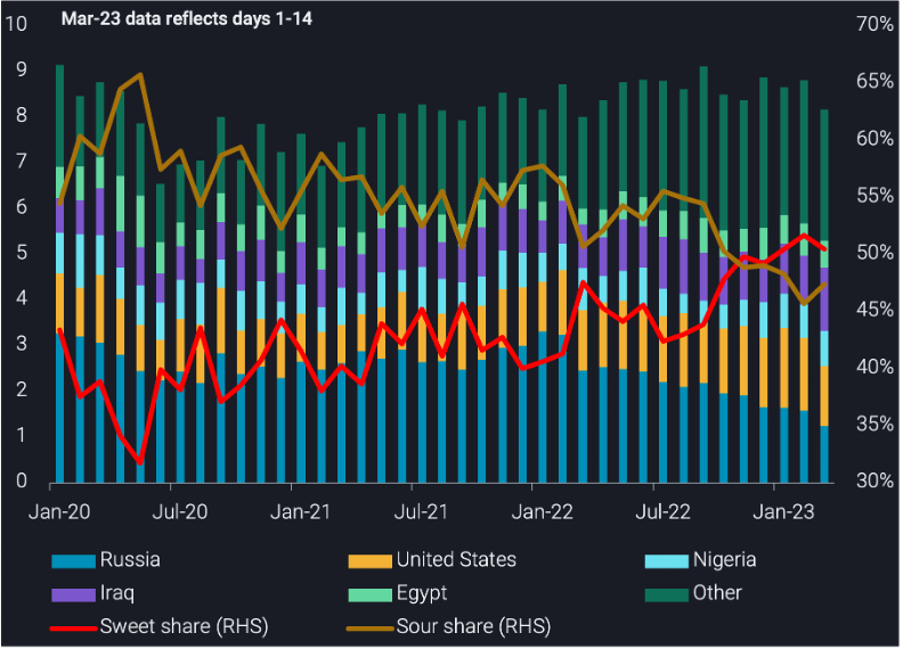

Europe’s crude/condensate imports declined 500kbd m-o-m in March (days 1-14), as imports from the US declined from their record-levels observed in recent months. This was marginally offset by an increase in crude imports from Iraq, which sit at multi-year highs in March so far.

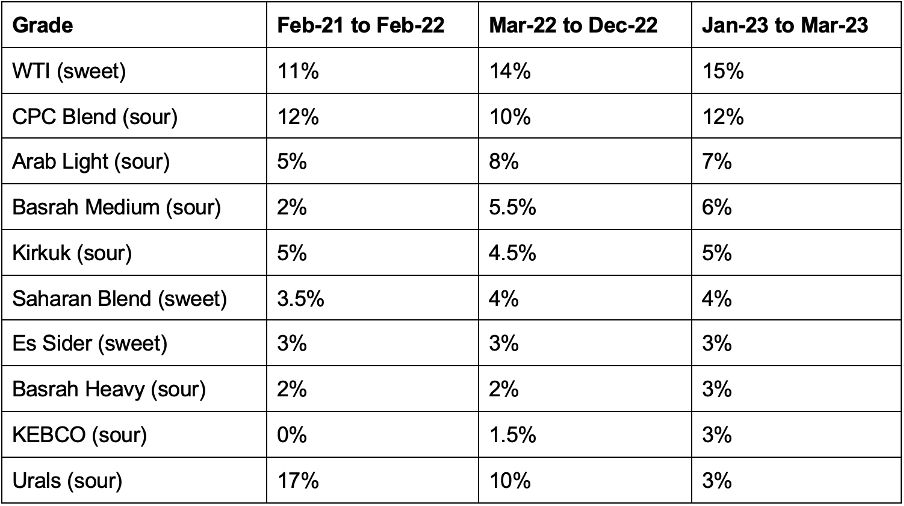

Europe’s crude/condensate imports have predominantly been sour, as Russian Urals (medium-sour) accounted for 17% of Europe’s total seaborne crude/condensate imports in the 12 months prior to the war (Feb-21 to Feb-22). This declined to 2% of Europe’s total crude/condensate imports since 5-Dec (average). This decline in Urals imports has driven the decline in the sour slate in Europe.

As Europe reduced its dependence on Russian Urals, it imported both sour and sweet grades as alternatives. This caused a shift in Europe’s crude slate, as sweet crude accounted for 52% of Europe’s crude imports as of February 2023, the highest proportion recorded according to Vortexa data and a 10 percentage-point increase y-o-y. On the other hand, sour barrels accounted for 46% in February.

Europe’s top-10 crude imports by grade and its respective share of Europe’s total seaborne crude/condensate imports.