Event Highlights: Vortexa brings Energy & Freight Insights Live to Geneva

Vortexa brought Energy and Freight Insights live to Geneva in celebration of the office opening in this beautiful financial centre on Thursday, November 28.

Our event which took place at Ritz-Carlton Geneva – Living Room Bar & Kitchen explored the latest trends shaping the energy and freight markets with a touch on 2025 outlook.

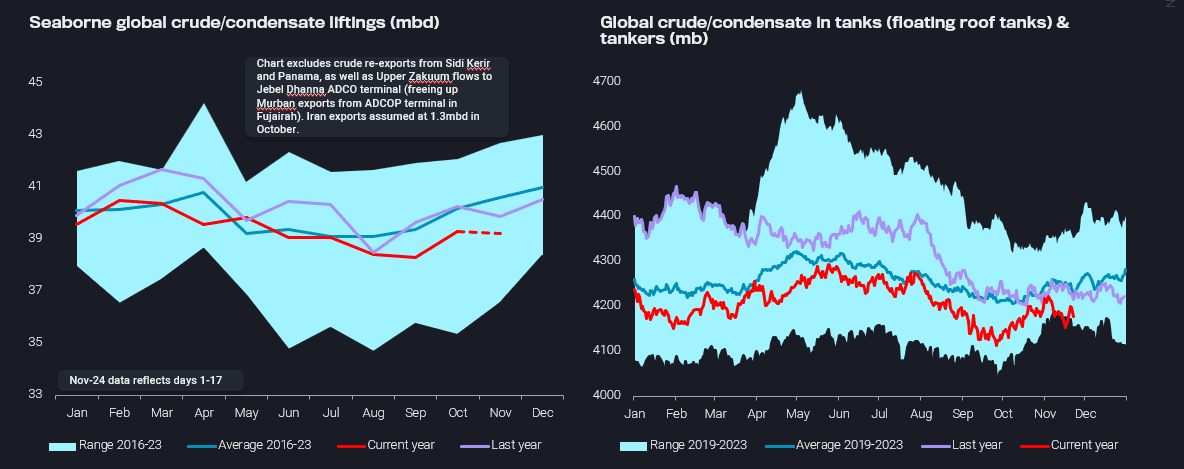

We started by looking at global crude and condensate liftings, which notably tracked below 2023 levels amid a backdrop of disappointing demand. Considering a year full of geopolitical tensions, with crude arrivals falling below last year’s levels for 9 out of the last 11 months, why have prices not moved further down? And if we look at the low volumes of crude/condensate in tanks and tankers, we can see that inventories have also been trailing below the five year seasonal average.

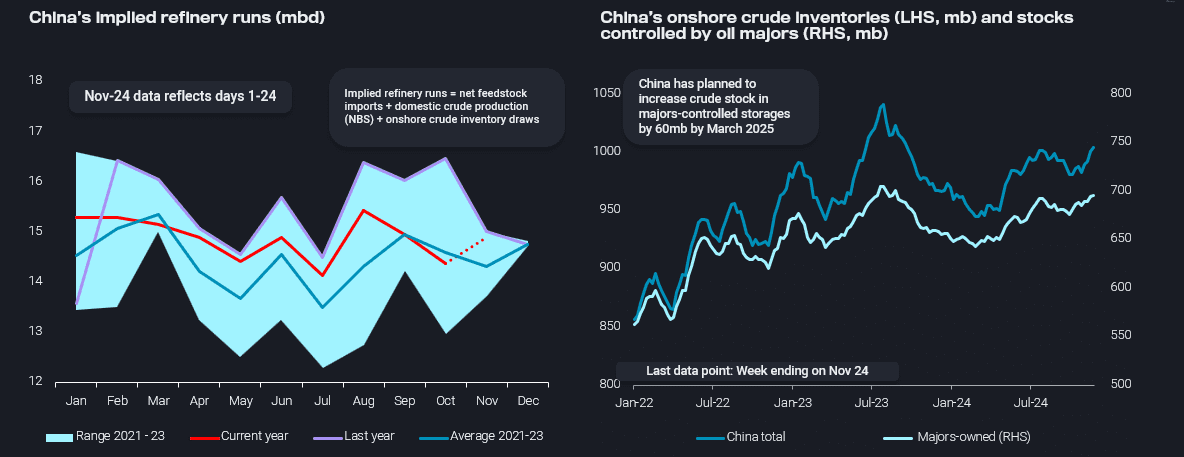

In addition to global crude liftings, we also reviewed the recent crude import rise into China where Chinese oil majors are stockpiling crude to meet recent SPR mandates, targeting an additional 60mb by March 2025 rather than increasing refinery runs. Since the program began in late September, 17mb of crude oil has been added to majors-owned tanks, contributing to a similar scale of build in the country’s overall onshore crude stock levels.

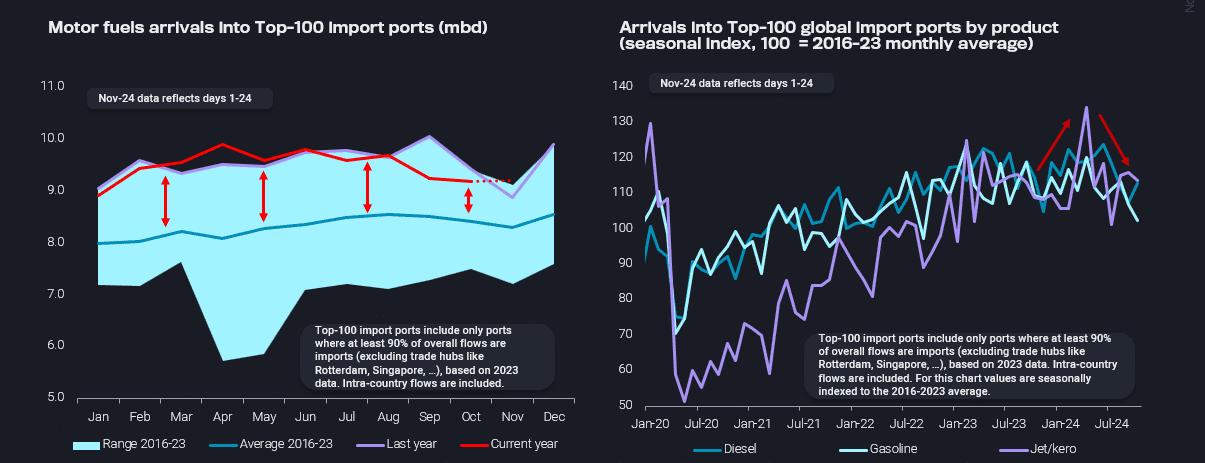

We then turned our attention to look at a snapshot of global demand indicators focusing on the recent decline in motor fuel demand shown by our top-100 import port demand indicators where 90% of all flows are imports (excl. trading hubs like Rotterdam, Singapore). This poor demand comes at a time when we are seeing high volumes of middle distillates coming into the European market alongside declining gasoline outlets culminating in a high pressure environment for European refiners which will likely conclude in more announced closures/consolidation.

We ended the discussion with a few bright spots in the market for 2025. Jet/kero import demand has picked up markedly over the last four months (Aug-Nov). Considering jet/kero production potential is limited by technical constraints and may be close to maxing out, it could highlight pricing upside for 2025.

Meanwhile fuel oil looks to be benefitting from low supply and high demand. The global crude slate has lightened substantially amid new refining capacity with high conversion capacity which has meant less fuel oil output. At the same time, growing demand for its use in power generation (Egypt) and the IMO 2025 changes starting in the Mediterranean effective May 2025 should also provide tailwinds.

After lots of networking, the Vortexa team regrouped in the morning for a breakfast debrief over fresh salmon and warm croissants!