How big is Europe’s crude dependency on Russia?

We will explore the not-so-easy answers to this question, with 8% to 24% being reasonable, depending on whether Russia-marketed seaborne crude is considered (sanctions approach) or whether all crude dependent on Russian infrastructure is included (real political/energy risk).

Europe’s dependency on Russian crude is a crucial factor in the oil market, especially as the December deadline in the European Union’s sanction package draws closer. By 5 December, all seaborne imports of Russian crude in EU countries, except for Bulgaria, have to cease completely. Pipeline flows via the Druzhba route can continue, albeit Germany and Poland, accounting historically for about two thirds of the volumes, have declared they will stop their pipeline imports as well.

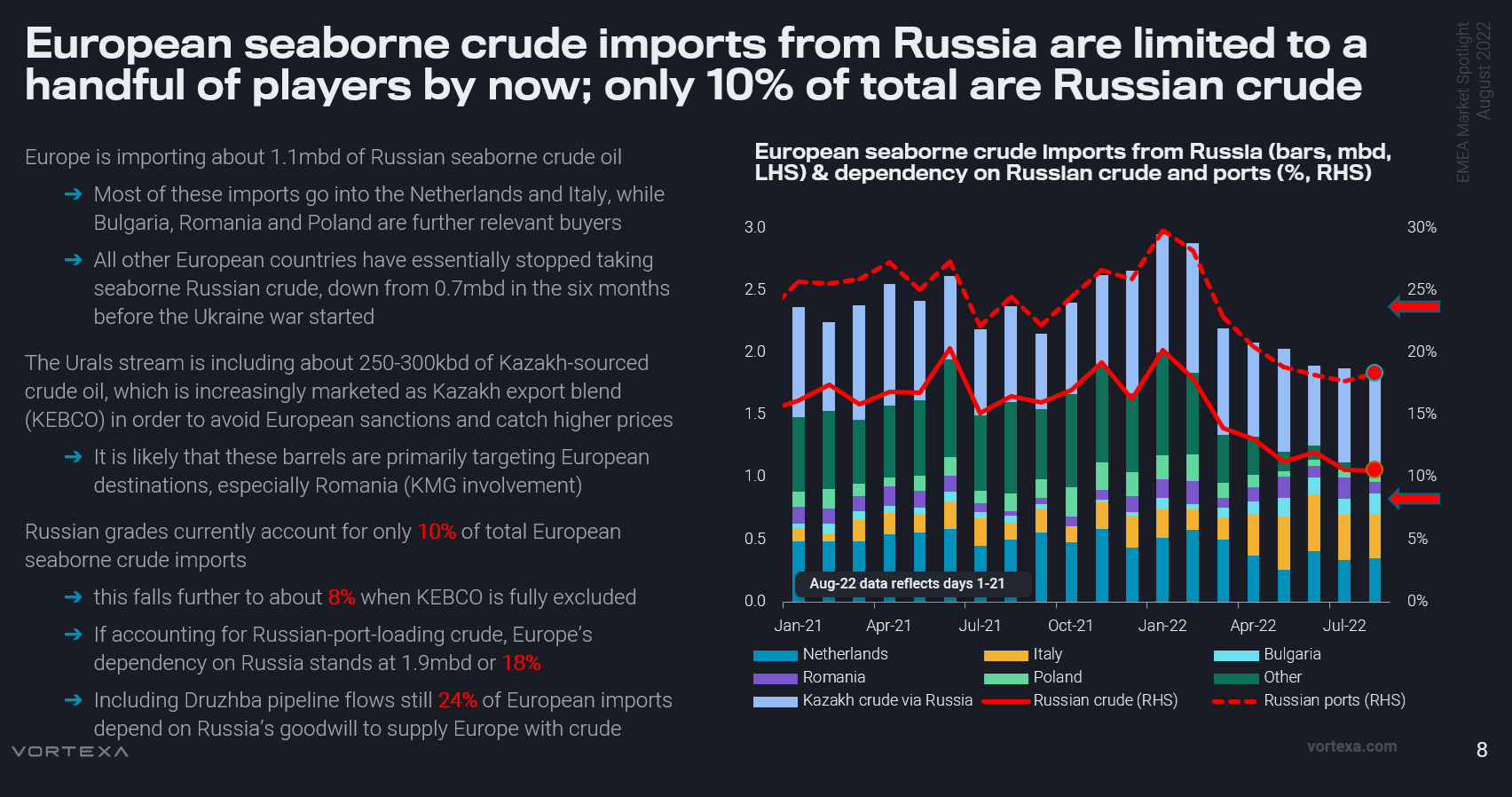

As of July and August 2022, Europe imports about 1.1mbd of seaborne Russian crude oil, mostly the flagship grade Urals, but also some Arctic and other grades. This figure does not include CPC Blend exports from the Russian port of Novorossiysk. In fact, all but five European countries have effectively stopped Russian crude imports already, after having taken an average 700kbd in the six months before the Ukraine war started. The remaining big takers are the Netherlands and Italy, while Poland, Bulgaria and Romania are accounting for the rest. These volumes make up slightly above 10% of Europe’s overall seaborne crude imports.

Infographic from our weekly EMEA Market Spotlight report

One of the complications in these calculations is that the Urals stream includes about 250-300kbd of Kazakh-sourced crude oil, as part of the widespread blending efforts to create one stable export blend and due to Kazakhstan’s limited overall export options. With the sanctions in place, these volumes are now increasingly marketed as Kazakh export blend (KEBCO), which also allows catching higher prices, albeit the quality is equal to Urals. It is likely that these barrels are primarily targeting European destinations, especially Romania given Rompetrol’s ownership by KMG. Imports of these volumes are in compliance with sanctions and reduce Europe’s dependency on Russian crude from that perspective to a surprisingly low 8% currently.

From a political and energy security perspective of course the dependency on Russia in terms of crude supplies remains much higher. If accounting for Russian-port-loading crude, specifically CPC Blend, Europe’s dependency on Russia stands at 1.9mbd or 18%. That Russia is able and potentially willing to disrupt the CPC Blend flows has been indicated by various disruptions on somewhat dubious grounds over recent months.

Including finally Druzhba pipeline flows, still 24% of European imports depend on Russia’s goodwill to supply Europe with crude. As for the southern leg of the Druzhba pipeline, to those countries that plan on continuing Russian crude imports, Ukraine as transit country has an important say in this regard as well, as illustrated by temporary stoppage of flows earlier this month.

European crude imports by source (mbd, 4-week average; external supplies, European supplies, Kazakh grades)

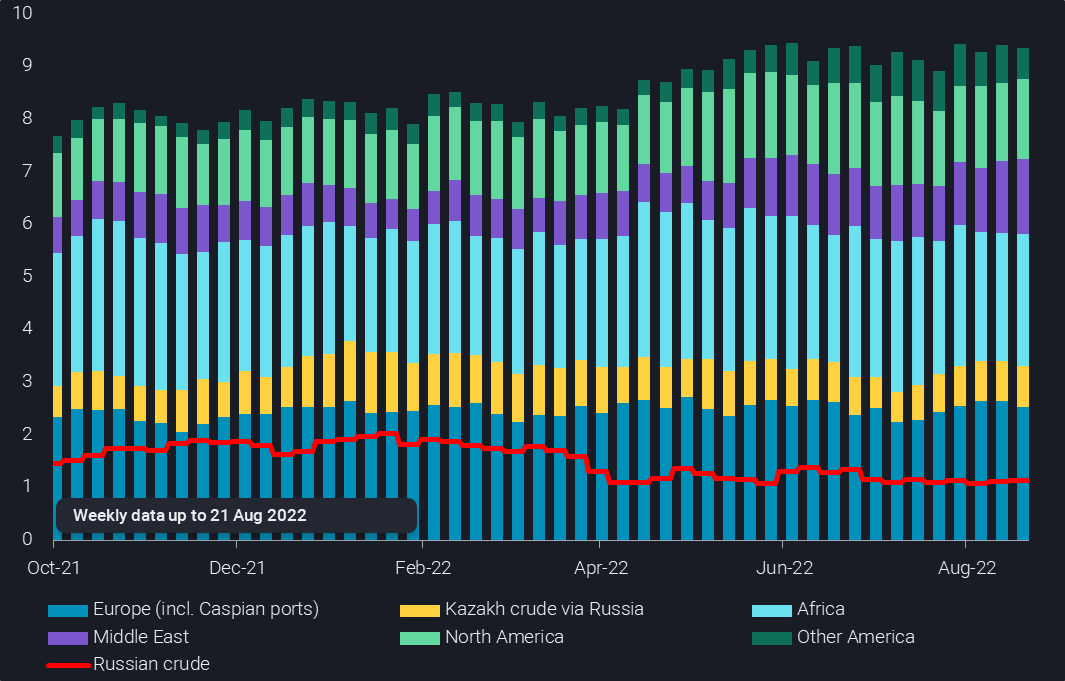

Getting rid of the remaining Russian crude volumes to comply with EU sanctions should be pretty easy from the European perspective, given ample alternative supply options. Next to regional North Sea, North African and Caspian supplies, West African and US barrels are also important components in the European crude import mix. US-to-Europe flows in particular are close to the historical high, with further upside left given ongoing SPR releases, steady albeit not spectacular shale output growth, and the upcoming refinery maintenance season. At the margin however, the biggest additions recently came from imports of more heavy and sour grades from Latin America and the Middle East, replacing the lost Urals crude more directly from a quality perspective.

In contrast, Russia may struggle more to find homes for all the barrels shunned by Europe. Total reshuffling needs may be about 1.1mbd, consisting of 700kbd of seaborne and 400kbd of pipeline flows to Europe. Turkey has already upped the Russian share in its crude imports, now close to 60% from less than 30% in 2020. Of course there may be further upside in flows to China and India, but only at substantial price discounts. Other countries have largely stayed away from Russian crude, at least so far, in spite of some claims of interest.

Perhaps this, in combination with currently lower outright prices, is increasing the chances of an implementation of the price cap idea. If so, this would in all likelihood eliminate the much more challenging need for Europe to replace Russian diesel supplies.