China recently issued an additional crude oil import quota of over 6mt to some independent refiners for the remainder of 2024, mirroring a similar approach last year. Recipients are expected to use the allowance for seaborne cargos with customs clearance by December 31, or for barrels drawn from bonded storage tanks.

However, not all qualified refiners have applied for the additional allocations. Many have been operating at low rates this year due to weak domestic demand, and the usual end-of-year quota shortage has fortuitously not materialised this time. Now, refiners who have been granted additional quotas may face challenges in completing the required volumes in time.

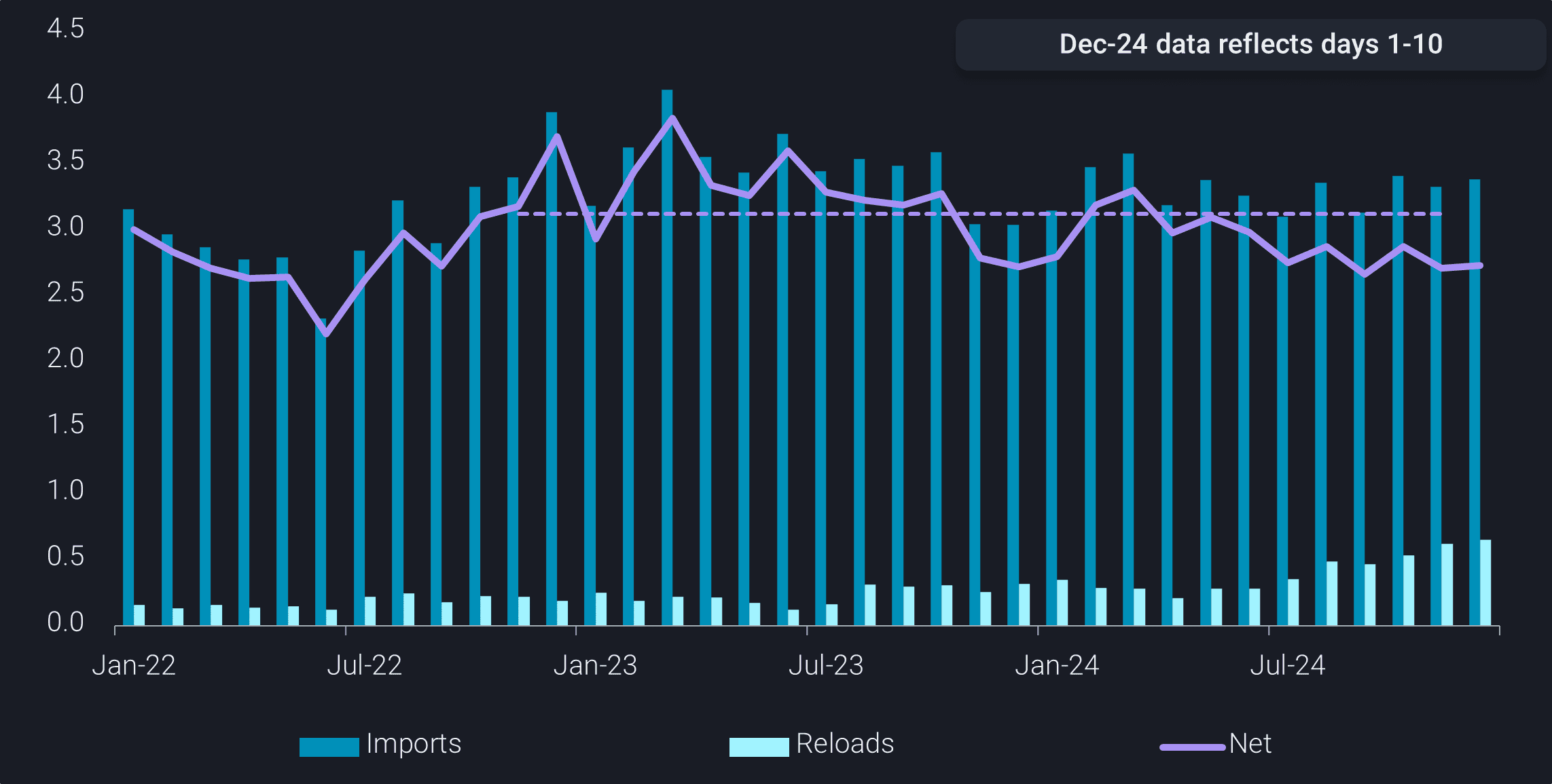

While Yulong’s start-up boosts overall refinery runs in Shandong, crude reloads from Shandong’s storage tanks for refiners outside the province have been increasing in recent months (earlier China blog). Shandong’s net feedstock (crude and residual fuel oil) imports stood at 2.7mbd in November, compared to the two-year average of 3.1 mbd, and this weakness is expected to continue into December.

Shandong net feedstock imports (mbd) – crude/RFO imports vs. reloads for non-Shandong

SPR stockpile reduces Russian ESPO supplies to Shandong teapots

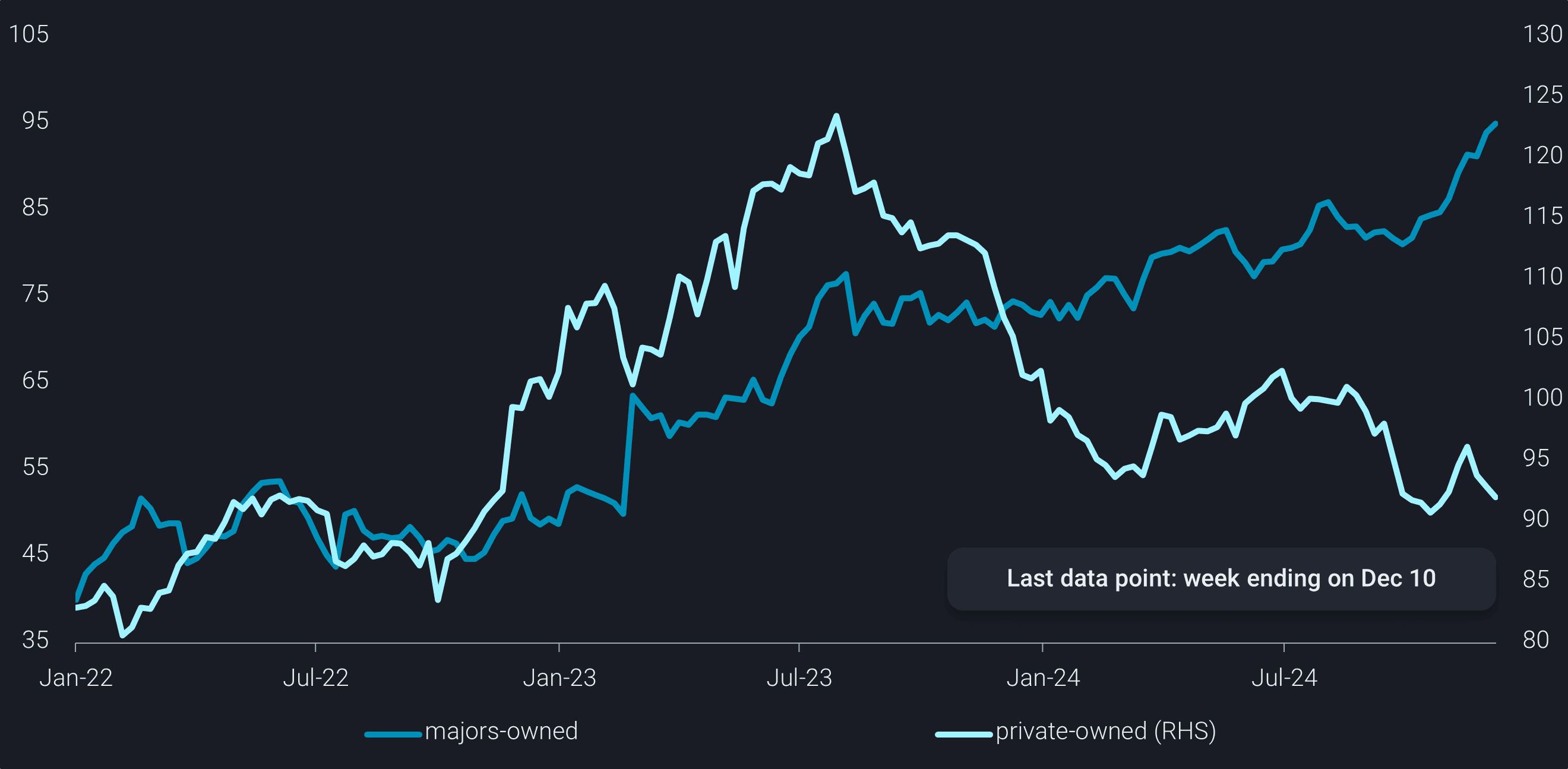

China’s stockpiling under the latest SPR mandate accelerated in November, with more Russian ESPO Blend crude and non-Iranian Middle Eastern grades added to majors-owned commercial storage tanks. Since the program began in late September, approximately 25mb of crude oil have been added to the tanks by the end of November, surpassing the total increase in the country’s overall onshore crude stock levels.

Oil majors are expected to achieve the 60mb target by March if the current stockpiling rate of 350kbd continues.

Shandong’s commercial crude stocks (mb) – majors-owned (LHS) vs. private-owned (RHS)

This will support tanker employment to some extent. However, without these stockpile efforts, China’s overall crude demand remains soft, which is suppressing the MEG-to-China (TD3C) and WAF-to-China (TD15) VLCC freight rates.

Additionally, Shandong teapots will continue facing ESPO tightness in the coming months. January ESPO cargos delivered ex-ship Shandong were settled at around $1.5/b above Brent futures, compared to discounts for September and October deliveries, according to market sources.

Heightened OFAC tanker sanctions on Iran put China’s December arrivals at risk

Recent US tanker sanctions have led to a slowdown in Iranian vessels calling at Shandong ports, as Chinese buyers increasingly require cargos to be delivered on non-sanctioned vessels.

Moreover, refiners are now preferring cargos carried by non-sanctioned VLCCs over other vessel classes, as the discounts on Iranian oil prices are already near the teapots’ tolerance levels, and freight costs have become a key factor in determining import expenses.

Iran is maintaining solid, or rather flat, FOB prices despite weakening benchmark structures, while Chinese refiners are bargaining discounts on their ex-ship cargos, narrowing the profit margin for middlemen, including ship owners, who bear higher risks amid the current OFAC sanction regime.

Currently, at least 191 VLCCs are serving sanctioned oil, with 78—about 40% of the dark fleet—on the OFAC sanctions list. Once a tanker is sanctioned, the ship owner is likely to sell it to Iran to serve as a floater, or alternatively, scrap the vessel.

Despite an abundant surplus of tonnage, ship owners may hesitate to deliver high-risk oil to China amid heightened US surveillance. This reluctance has led to delays, with some October orders only being delivered in November, while some November cargos remain undelivered as of the report date.

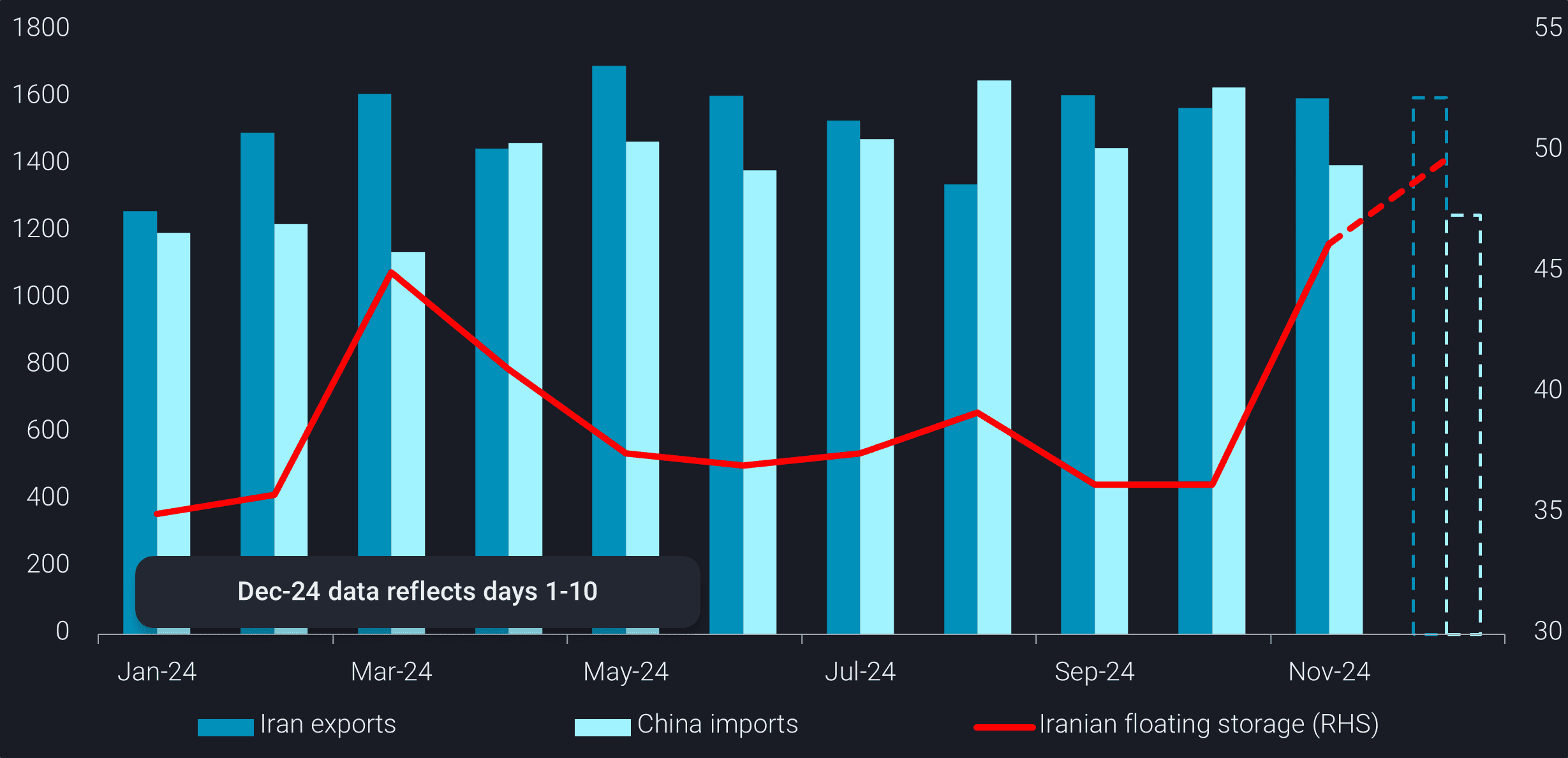

Iran crude/condensate exports, China imports (kbd, LHS) and Iranian floating storage (mb, RHS)

Iranian oil on water has been rapidly accumulating, with 46mb floating in the Persian Gulf or South China Sea as of December 2. Iranian floating storage offshore Singapore has surged to a multi-year high, exceeding 40mb, and is still building.

Iran is expected to eventually offer higher profit-sharing to ship owners to fulfill refiners’ orders and free up floaters, especially given the uncertainty surrounding its supply agreement with Syria. However, this may not occur as soon as 2024 concludes, as Chinese buyers are under pressure to utilise their crude import quotas.