Greek operators return to the Russian crude trade, leaving a vacancy in the Atlantic Basin Aframax market

We examine vessel repositioning from the Russia Baltics/Black Sea to the Russia Far East. A wide variety of Greek-operators are beginning to fill the gap left by OFAC sanctions for the flows going to India and Turkey, pointing to steep discounts in Russian crude going to these markets.

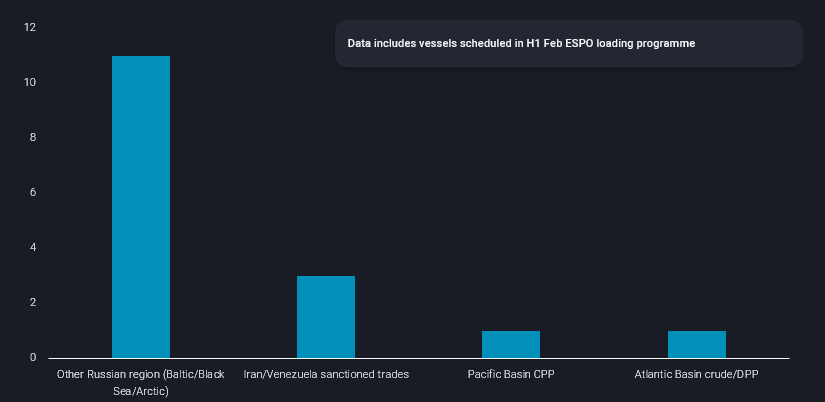

Russia is prioritising the ESPO trade from Russia Far East to China. S&P, “clean” vessels (non-OFAC sanctioned) repositioning from the Russia Baltic and the use of “clean” vessels from Iran/Venezuelan trades are all tactics demonstrating Russia’s commitment to get ESPO barrels to China.

Vessels which have joined the Russian ESPO trade after 10 Jan OFAC sanctions by previous trading history (no. of vessels)

What about crude exports from the rest of Russia (Baltic, Black Sea, Arctic)?

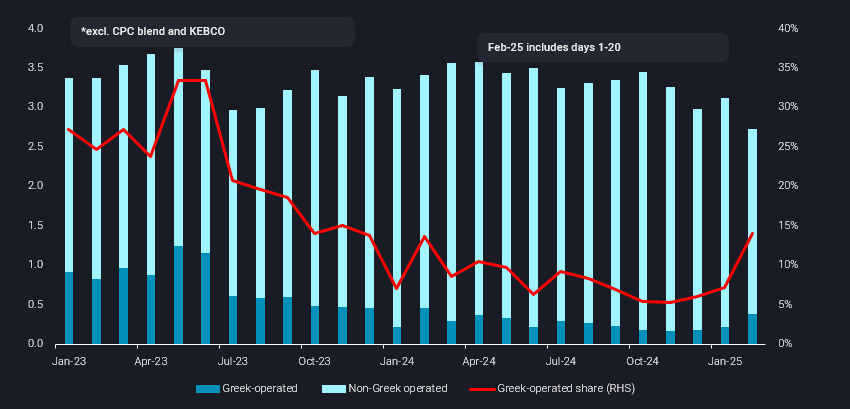

Excluding CPC and KEBCO, Russian crude exports from outside of the Russia Far East comprise about 65% of Russian crude exports. As we discussed in our exclusive report on the 10 January OFAC sanctions, the number of non-OFAC-sanctioned vessels available to lift crude above the price cap will be inadequate to also cover Russian Baltic/Black Sea exports to India and Turkey when Kozmino-China is being prioritised.

STS operations from a sanctioned vessel to a non-sanctioned vessel are less likely by Indian and Turkish buyers due to their stance on OFAC compliance. Russian crude exports to India and Turkey will need to be offered below the price cap so that Greek operators can facilitate these volumes.

Preliminary February data (days 1-20) is showing Russian crude volumes carried by Greek operators at a 12-month high, indicating this is already materialising.

Russian crude* exports by vessel operator nationality (mbd, LHS) and Greek-operated share (%, RHS)

Greek operators enticed by deep discounts

When looking at the profile of some of the Greek operated vessels which lifted Russian crude since 10 January, the wide range of operators is surprising. The average vessel age is 12, with 26% of these vessels 5 years or younger. This demonstrates there is no barrier to entry in terms of age.

Furthermore, 60% of these vessels had not carried Russian crude (excl. CPC/KEBCO) for 6 or more months, with 15% of the vessels without a Russian crude voyage since 2023. Two vessels have lifted Russian crude for the first time, both of which were recently active in Europe and the US Gulf. This behaviour points to Russia’s need to offer a discount to ensure exports continue and could also point to high effort at OFAC compliance on the part of the likely buyers of these cargoes in India.

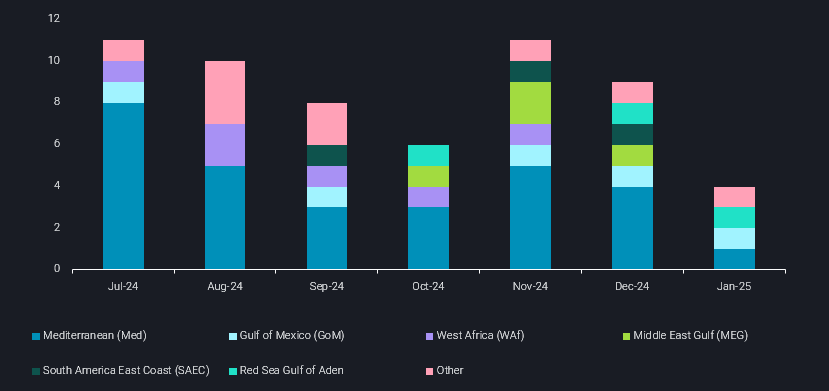

These Greek-operated vessels have migrated out of mostly Atlantic Basin trade, especially in the Med (see below chart). This could lead to significant tightening in Atlantic Basin Aframax supply, and higher earnings for vessel operators in those regions.

Previous voyages (excl. Russian origin) by shipping region of Greek-operated vessels which have lifted Russian crude after 10 January (no. of vessels). Retrieved via Freight API/SDK

What’s next for the tanker market?

Too many questions remain around the timeline of a potential Russia-Ukraine ceasefire to speak concretely, but what is likely is that an unwinding of these flows will be more gradual, with some still going East. Regardless of whether OFAC removes sanctions on some vessels, older vessels or those not maintained may find it challenging to re-enter the mainstream trade.

Eventual scrapping or S&P to facilitate sanctioned volumes (from Iran/Venezuela) offshore Singapore and Malaysia is most likely. With the US “maximum pressure” campaign beginning around Iranian exports, and the Chinese appetite for discounted barrels not retreating, it is undeniable that the logistics of the sanctioned trade will keep the demand for “clean” (unsanctioned) tonnage elevated.