MR tankers in 2025: Geopolitical and market drivers bring European MRs back into the spotlight

In this piece we will explore the main drivers for the current price trajectory of MR tankers across the globe and what indicators tell us about the future

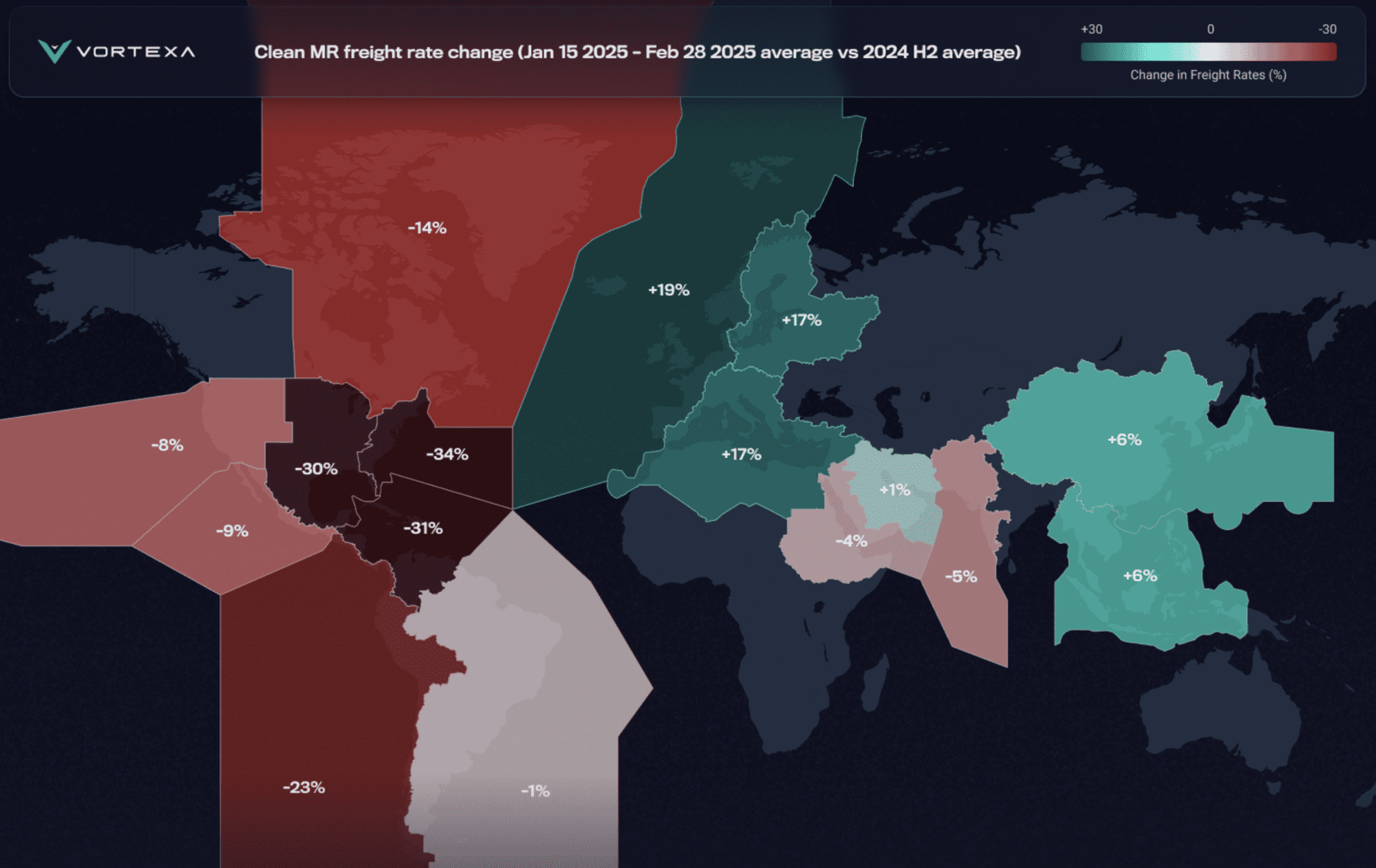

The first two months of 2025 have been marked by significant geopolitical shifts—new sanctions on Russia-linked vessels, an Israel-Palestine ceasefire, and the announcement of US tariffs on Canada and Mexico—all of which look set to reshape the freight market. To assess their impact on the MR market, we are quantifying freight rate changes worldwide from January 15 onward, compared to the second half of 2024.

Powered by Anywhere Freight Pricing

To understand the global impact on MRs, we leveraged Vortexa’s latest innovation, Anywhere Freight Pricing. More than 150 routes were used to create the chart above, illustrating a comprehensive market view. A glance at the data reveals that MR tankers in the Pacific have outperformed their H2 2024 levels, while in the Atlantic, trends diverge between Europe and the Americas. Although geopolitics have played a role—directly or indirectly—current freight rates are primarily driven by regional supply and demand fundamentals.

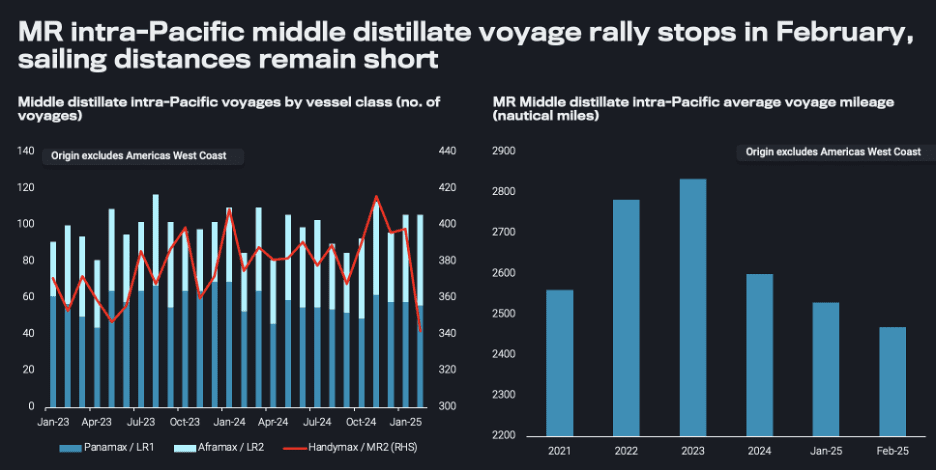

Short-haul voyages dominate in the Pacific, but MR strength fades in February

In a previous freight-focused blog, we examined the decline in East-West LR utilisation, which has ultimately bolstered demand for smaller tankers, such as MRs. Instead of heading West, middle distillates from the Wider Arabian Sea (mainly Middle East and India) have supplied nearby markets such as East Africa, supporting MR activity on the TC17 (Middle East to east Africa) route, specifically in Q4 2024 and the start of Q1 2025.

Meanwhile, Wide Arabian Sea exports to Oceania—predominantly on LRs—have largely confined Northeast Asia-origin MRs to operate regionally. This has overall contributed to a global MR trend where the short-haul nature of voyages is capping tonne-mileage.

February’s sharp drop in MR employment further clouds the tonne-mile trajectory in the region. An open East-West diesel arbitrage could redirect supplies to the Atlantic, effectively creating marginal long-haul opportunities for MRs in the Pacific, supporting utilisation. In the medium-term, however, with Europe’s winter demand fading and refineries returning gradually from maintenance in April, a persistent resurgence in MR voyage mileage appears rather unlikely.

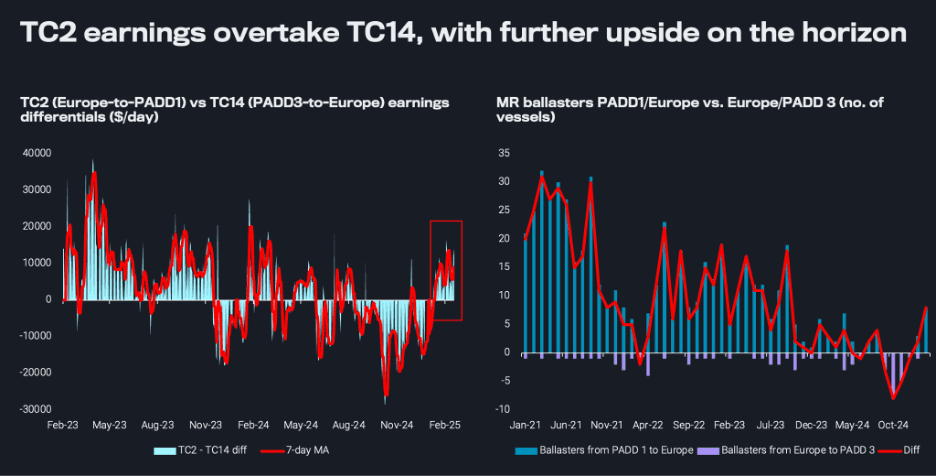

Russian voyages and tariff applications will continue to benefit MRs out of Europe, unlike the US Gulf

In the Atlantic, TC2 (Europe to PADD 1) MR earnings have consistently outperformed TC14 (PADD 3 to Europe) earnings for the first time since summer, effectively restoring TC2’s status as the region’s primary front-haul. As a result, more tankers are now ballasting back to Europe after PADD 1 discharge, rather than seeking cargoes in PADD 3. MR employment in the US Gulf, however, may remain subdued. This is initially due to refinery maintenance but could, in the medium term, come from potential run cuts as tariffs increase costs for US refiners.

Conversely, certain factors could continue to support MR tankers out of Europe. On the supply side, MR availability in the region may stay tight, as strong Russian diesel exports from the Baltic reduce competition for mainstream cargoes in the Mediterranean and Northwest Europe.

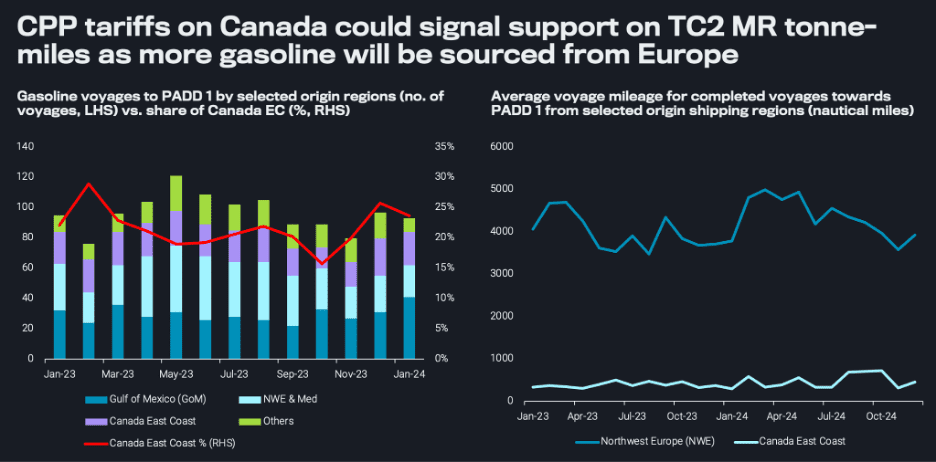

On the demand side, US tariffs could provide further support. Roughly 25% of all gasoline voyages to PADD 1 originate from East Coast Canada. With a 10% tariff imposed on Canadian products, buyers may shift toward European gasoline, supporting tonne-miles, as the Europe-PADD 1 route is ten times longer than the short-haul Canada-PADD 1 trade.

Canadian gasoline could go instead to the Caribbean, potentially to be blended with PADD 3 gasoline for delivery on non-Jones Act tankers to PADD 1. Canadian diesel may go to Europe instead, with at least one diversion from the US already observed. Some participants think that Canada East Coast – PADD 1 flows will just continue and the extra-costs will be shared between buyers and sellers, and this may especially initially be the case. But 10% is close to $10/b for gasoline and diesel currently, opening up a lot of space for additional logistical operations, providing new opportunities for traders and tankers.