China’s LPG demand resilient despite economic headwinds

China’s LPG demand has surpassed market expectations with suppressed VLGC freight rates supporting robust imports.

China’s LPG imports have surpassed market expectations this year despite the country’s gloomy economic outlook. The country’s seaborne imports in July set a record-high of 1.4mbd, and total imports in the first eight months of this year are up nearly 10% year-on-year.

Incremental supplies have come from the US, with imports rising by almost 35% between January and August. Imports from the Middle East are down 9% in the same period, driven by lower supplies from Qatar and Saudi Arabia. Iranian supplies have largely held stable so far this year, averaging 270kbd.

Against a backdrop of weak margins, six new PDH plants with a combined capacity of 4.2MPTA have started up so far this year. 750kTPA Shandong Zhenhua Petrochemical PDH plant was the latest unit that came online, achieving on-spec production in early August. The new 660kTPA Guoheng Chemical PDH plant is expected to start in Q3/Q4 and is likely to be the final one for this year.

Whilst China’s LPG import momentum is expected to continue through the rest of the year, optimism for further growth has been dampened by a few factors. Underlying weakness in PDH margins, which have kept several less competitive plants shut for prolonged periods, downside risks from ethylene crackers shifting towards naphtha as feedstock amidst the narrowing LPG-naphtha spread. Butane demand for gasoline blending may see an uptick ahead of China’s Golden Week in October, but gains could be offset by losses from petrochemical demand.

VLGC freight rates see limited recovery with ample tonnage supply

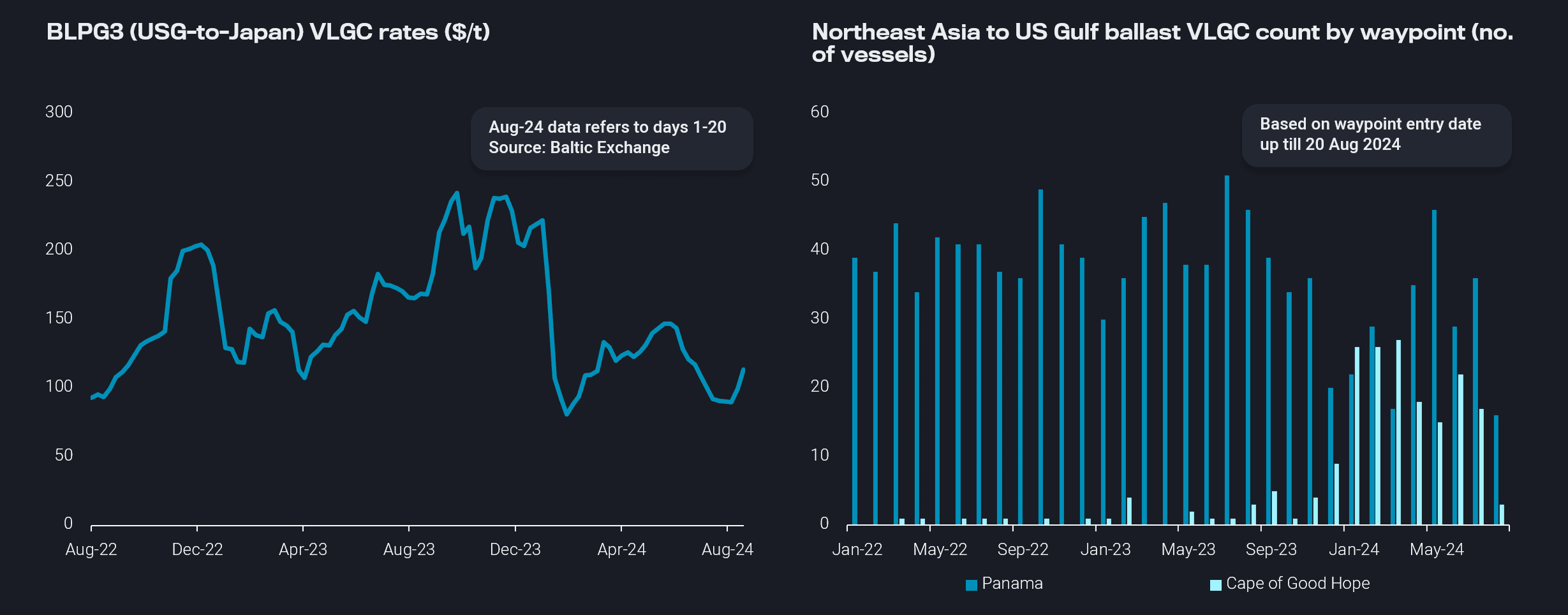

Weaker VLGC freight rates have also supported China’s robust LPG imports this year. BLPG3 US Gulf-to-Japan VLGC rates were on a continuous decline from June and reached near multi-year lows in early August, before rebounding over the past two weeks off the back of increased fixing activities.

The easing of Panama Canal transits has seen a rebound in southbound traffic, cutting US Gulf-to-Northeast Asia VLGC voyage times leading to increased tonnage supply. However, some vessel owners still prefer to transit via the Cape of Good Hope for the return journey from Northeast Asia to the US Gulf. The addition of 23 newbuild VLGCs this year have further expanded the VLGC fleet, keeping tonnage supply ample and in turn, limiting the recovery of VLGC freight rates.

Download our latest LPG Special Report Q3 here to read the latest developments in the global LPG flows and freight market.

Left: Northeast Asia to US Gulf ballast VLGC count by waypoint (no. of vessels), Right: BLPG3 (USG-to-Japan) VLGC rates ($/t)