Robust global LPG supply, export growth expected, challenging netbacks

Global LPG supply and exports are expected to surge in the coming months, led by returning Middle East production and US terminal expansions. Iranian material looks resolute despite “maximum pressure” measures, while an uptick of Russian barrels is looking like a distinct possibility.

Global LPG supply and exports are looking ample heading into the seasonal spring demand lull and well into summer, as we have indicated in our recently released LPG special report. Indeed, preliminary March exports are looking robust from a y-o-y perspective with the major exporting regions firmly in positive territory.

The second quarter of the year is likely to prove no different. Although refinery maintenance in both east and west of Suez will curtail refinery output of LPG, field production is apparently on the rise. OPEC+ is expected to begin slowly unwinding production cuts in April and North Sea planned gas plant maintenance looks relatively light through in the second quarter with the Kaarsto plant going down in late March through early April. In the US, producers will be gearing up for increased LPG export terminal capacity expansions in the summer.

Given the quarterly levels of export growth in recent years, Q2 2025 exports should average around 4.92 mbd mark, up by 4% y-o-y, largely from the US and Middle East; second quarter five-year averages are around 4.7 mbd, Vortexa data show.

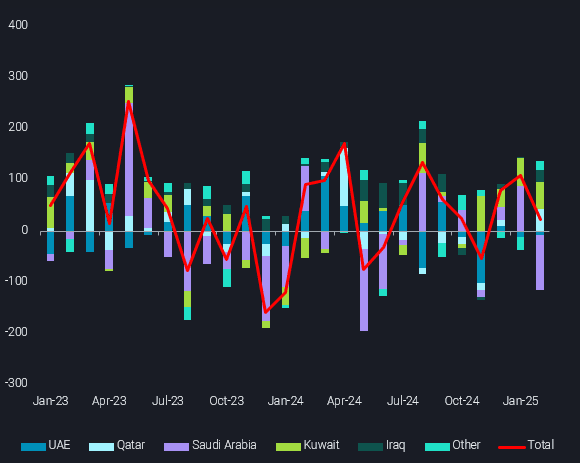

Middle East supply rollbacks little impact LPG sendout; Iran exports steady

In early March, OPEC+ agreed to resume unwinding its cumulative 2.2 mbd crude production cuts from late 2022, over an 18-month period. These 137 kbd sequential increases on the oil side are scheduled to begin in April roughly, translating to about an additional VLGC’s worth of Middle East LPG exports. For context, the region (excluding Iran) exported 1.25 mbd of LPG on average last year, equivalent to about 68 VLGCs per month.

The largest increases are likely to come from Saudi Arabia and UAE with the latter’s Al-Hosn gas plant– completed last year — being more fully utilised once cuts are unwound.

Non-OPEC member Qatar will continue to surge its LNG-driven production this year, but greater associated LPG volumes will be unleashed in 2026 with the expected North Field East expansion.

Some of the region’s export increases will be tempered by Iran, given the ongoing “maximum pressure” measures by the US in an attempt to drive the country’s crude exports to zero. As expected, these measures have slowed, but not stopped, Iran’s LPG exports. Vortexa preliminary data shows Iran’s February LPG exports at 269 kbd, down by 49 kbd m-o-m with all sendout heading to China. China’s continued willingness to take heavily discounted Iranian barrels, despite the Shandong Port Group’s ban, is quite evident as the province’s February LPG imports from Iran was up by 15 kbd m-o-m at 51 kbd. Our market soundings indicate these bargain-basement barrels are in hot demand as Chinese PDH margins continue to languish below the $150/t breakeven levels, according to our in-house forward margins calculations.

Year-on-year change in Middle East (excl. Iran) LPG exports by origin country (kbd)

US terminal expansions to ensure increasing market share; elevated sendout

US LPG exports have been straining at capacity limits, with terminal utilisation rates averaging near 95% so far this year, up by nearly 2 percentage points y-o-y. US NGLs and LPG production rose 513 kbd and 212 kbd y-o-y respectively last year (a sequential increase of 8% and 6.9%), per EIA data. Given initial US producer guidance so far, it is reasonable to assume 2025 y-o-y growth rates of 7% and 6-6.5% for NGLs and LPG respectively this year, meaning US sellers are highly incentivised to push as much material as possible on the water.

To that end, the following US LPG terminal capacity expansions are on tap over the next few months:

- Energy Transfer Nederland in Q3 2025 (250 kbd NGLs with presumably 160 kbd of that pegged for LPG)

- Targa Galena Park in Q4 2025 (22 kbd)

Larger LPG expansions – Enterprise Neches River (as much as 360 kbd for LPG) and Enterprise Houston (300 kbd) – are expected in H1 and H2 2026 respectively, ensuring US LPG continues charting record sendout.

Potential increase of Russian LPG possible; Turkey likely to absorb additional supply

A wildcard in the months to come is incremental Russian LPG exports with the backdrop being a potential ceasefire with Ukraine. Since the European Union formally imposed sanctions on Russian LPG in December 2023, several countries began boycotting Russian material since the invasion in February 2022, driving annual exports to plummet to 26 kbd on average last year. That said, so far this year, LPG exports have averaged around 32 kbd.

A return to historical highs of above 100 kbd is unlikely given what we believe is an overall degradation of the Russian refinery system and a lack of upstream investment as the nation diverted its capital towards its military complex. That said, a return to pre-war levels of 40 kbd on average may not be out of the question. Turkey is likely to absorb the additional supply as it remains to be seen whether Northwest Europe would significantly increase its intake of Russian exports should the EU adopt a more aggressive military stance towards Russia.