Atlantic Basin diesel fundamentals point towards excess supply

Diesel flows to the Atlantic Basin have surged to seasonal highs on multiple occasions in 2024, with the same trend continuing in early 2025. Last year, high run rates in the US Gulf, steady exports from East of Suez refiners and an increasing volume of Russian barrels reaching the South Atlantic were just some of the factors contributing to ample supplies to net-importers in Europe and Latin America.

Competing export flows indicate a well-supplied market

Late 2024 marked a strong shift in Middle East diesel exports from West to East (read more here), leaving Atlantic Basin importers with the lowest seasonal diesel barrels available from East of Suez in over three years.

In response to the gap created by seasonal pricing incentives in Asian markets, diesel exports from North America surged to a five-year seasonal high in the fourth quarter, 18% higher y-o-y. The chart below reflects that North American diesel rapidly captured the market share in the last quarter of 2024, indicating ample prompt diesel availability. Diesel stock levels in PADD 1 and ARA began rising during this period (EIA, Argus), highlighting a weak absorption of imports. This flow slowed as PADD 3 entered into its refining maintenance season, partly due to Middle East refinery outages further reducing available volumes.

Now, as PADD 3 exits its maintenance season, Middle East barrels are returning to the Atlantic Basin market, boosting overall supply levels and pressuring diesel margins.

European refinery shutdowns might not be enough to bridge the demand gap

As we look forward amid an oversupplied product market toward 2025, we know that Europe is anticipating the loss of at least 300kbd of refining capacity in the second quarter, on top of the 80kbd already lost at the Gunvor Rotterdam refinery last November. CDU closures at the Wesseling (147kbd) and Grangemouth (150kbd) refineries provide upside potential for refined product imports from outside regions.

Vortexa data shows that core Europe diesel imports from outside regions in the first quarter 2025 are down 5% y-o-y (Core Europe includes European Union, Norway, Switzerland and UK). Given expectations of permanent refining capacity loss and a surge of unplanned outages hitting the region, import levels have shown relative weakness. At the same time, ARA inventories remain well above last year’s levels (Argus), indicating that the extra imports in March, intended to cover domestic shortfalls, are not for immediate consumption.

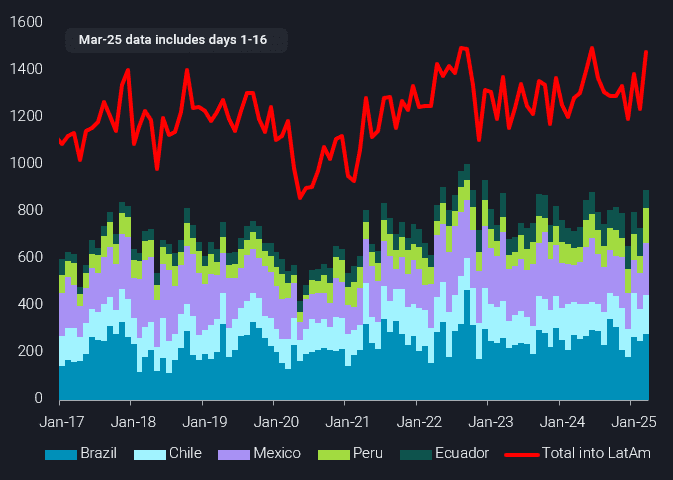

Latin America demand is not enough to tighten the market

Meanwhile, LatAm diesel imports remain robust, with Vortexa data showing a 6% increase in the last four quarters relative to the same period last year. Brazil’s strong agricultural demand continues to attract cheaper long-haul Russian diesel shipments, while PADD 3 diesel continues to redirect toward the Panama Canal to supply Chile and Ecuador’s increasing demand in power generation.

Even if the trend continues, this modest growth in imports is likely not enough to absorb excess Atlantic diesel supplies. Further upside potential in this region is limited by increased biodiesel adoption and ongoing fiscal consolidation.

LatAm diesel/gasoil imports by selected countries/territories and total imports (kbd)

Looking forward, PADD 3 diesel exports continue to compete with Russian barrels and East of Suez supplies for market share.

At the same time, the world watches the ramp up of two large refineries in the Atlantic Basin. Nigeria’s Dangote refinery (650kbd), running currently at an estimated 60% capacity, is expected to produce 150kbd of on-spec diesel/gasoil with 100kbd available for export. The Dos Bocas refinery (340kbd) is targeting 120kbd of diesel/gasoil for the domestic market.

The likely result of further supply coming into the Atlantic Basin market is further downward pressure on diesel cracks until a fresh round of refinery shutdowns tightens the market once again.