Atlantic Basin motor fuel arrivals fall for the fifth consecutive month in January

We take a look at Atlantic Basin motor fuel arrivals at a time when motor fuel loadings in the region reach the top of the seasonal range amid expanding refinery capacity in the South Atlantic and declining demand outlets.

Atlantic Basin motor fuel (gasoline, diesel) arrivals fell for the fifth consecutive month in January 2025 to 8.5mbd. Despite steep declines in the Wider Med, Wider Northwest Europe and the South Atlantic (where arrivals slid 12% from their peak in August 2024 to January 2025), an increasing trend in motor fuel arrivals can be seen when looking at the North America East Coast region.

Motor fuels head to the Caribbean

As motor fuel arrivals declined in most of the Atlantic Basin, the wider North America East Coast (Canada East Coast, Caribbean, Gulf of Mexico and US Atlantic Coast) reflected an overall rising trend in motor fuel arrivals between October – December 2024.

However, the growth was not underpinned by the dominant regional pillars of demand (USAC, East Coast Mexico) but instead by strong imports into the Caribbean where gasoline flows from North America surged by 19% from Sept-Dec 2024 compared to the same period in the prior year, reaching an equivalent share to the USAC and East Coast Canada in January (broken red lines). This redirection of flows signals a desperate need for gasoline producers to find outlets amid an environment continually chartacterized by low demand and prolific supply.

Motor fuel imports into East Coast Mexico and Nigeria reach multiyear lows in the new year

Amid rumbings of the Dos Bocas refinery (340kbd) start-up in East Coast Mexico, the region hit a multiyear low in motor fuels arrivals in January 2025 dropping to 416kbd, the lowest level since February 2022 (312kbd). However, despite only processing 43kbd in December-24 (Pemex), it is likely that the 18% m-o-m boost in motor fuels production from Pemex refineries in December is the main cause for the recent decline in imports (Argus Media).

Unlike the Dos Bocas refinery, the Dangote refinery (650kbd) on the opposite side of the Atlantic Ocean in Nigeria continues to ramp up gasoline production despite recent problems with the RFCC unit. As a result, gasoline imports into Nigeria have hit the lowest level since January 2017. The increase in gasoline production from Dangote combined with Port Harcourt (210kbd) refinery restart will likely keep a lid on gasoline imports to the region for most of 2025 causing NW Europe to look for other outlets in which to redirect its growing inventories.

However, as we approach the likelihood of the US placing tariffs on petroleum imports from Canada and Mexico, we could realistically see some opportunities for European suppliers toward the USAC opening up.

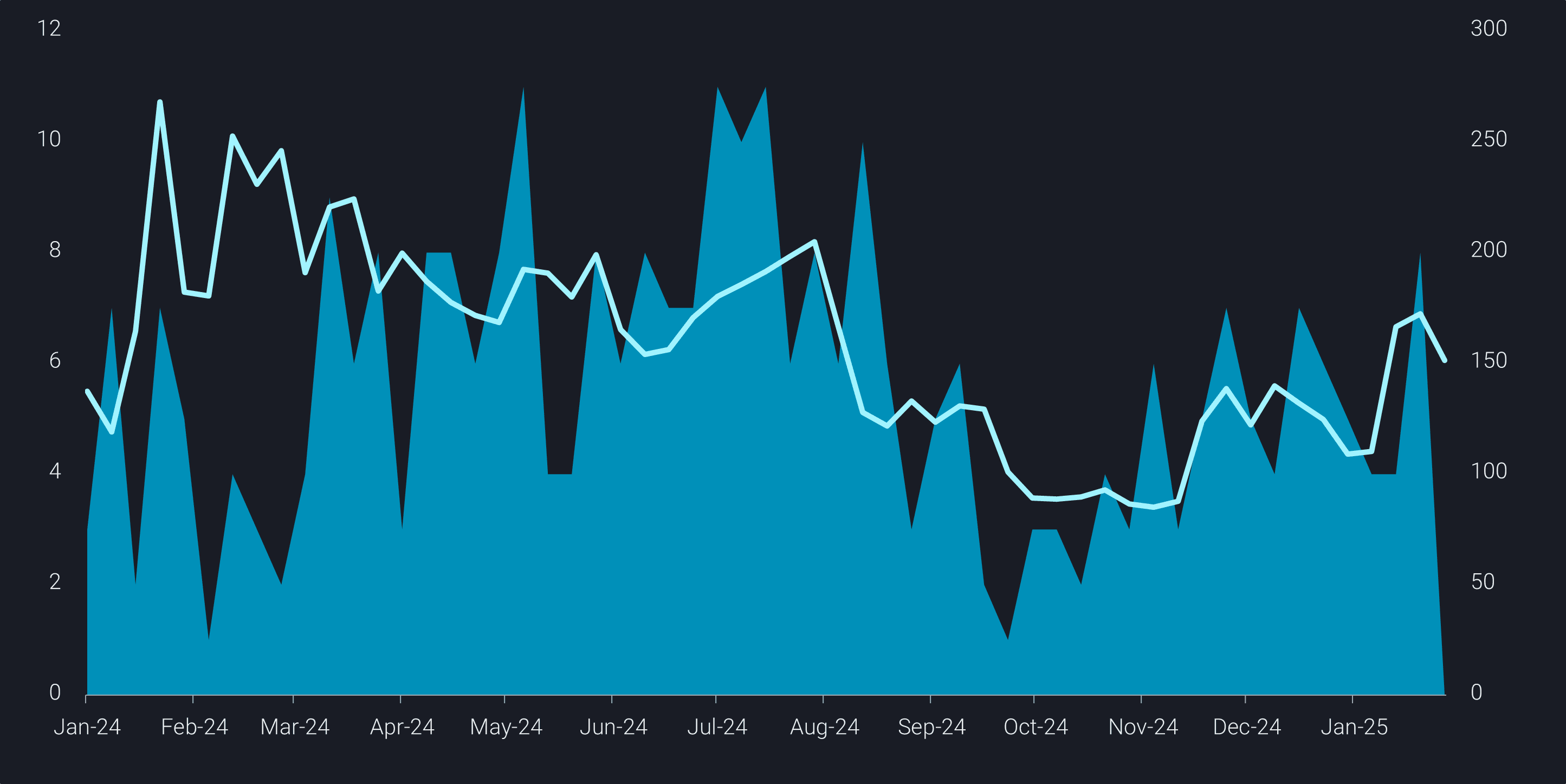

MR gasoline voyages from Northwest Europe to the US Atlantic Coast rose recently at a time of historical lows for gasoline exports out of the ARA region. Gasoline loadings in Northwest Europe pointed toward the US Atlantic Coast nearly doubled week-on-week despite gasoline stocks in PADD 1 looking healthy for this time of year. ARA gasoline stocks reached their highest level since at least 2011, also serving as a push factor, however there is a strong possibility that this type of counter seasonal buying is a response to the looming tariffs likely to make Canadian gasoline into PADD 1 more expensive (alongside US gasoline production as well).

MR voyages from Northwest Europe to US Atlantic Coast (no. of voyages, LHS) and TC2 rates (avg weekly $/ton, RHS)