Global dirty product arrivals remain scarce despite surge in Asia HSFO cracks pulling in arbitrage flows

The latest surge in Asia’s high sulphur fuel oil cracks have pulled in arbitrage flows from Russia and Middle East to Asia on improved arbitrage economics. However, the slowdown in global dirty petroleum products arrivals will likely continue, reflecting the changes in the global refinery landscape.

Global high sulphur fuel oil (HSFO) cracks have recently strengthened, with Asia’s HSFO cracks being the most prominent. Asian HSFO cracks reached an eight-month high at -$0.3/bl on 11-February (Argus Media). The movement close to parity was influenced by the threat of potential shortages of HSFO from disruptions due to Office of Foreign Assets Control (OFAC) sanctions placed on Russian and Iranian tankers. However, OFAC sanctions are unlikely to significantly lower Russian residual fuel oil exports as western operators will likely be able to enter the Russian dirty product trade, given that prices trade under the price cap. (Read more from our Russia residual fuel oil blog).

Russia has directed more residual fuel oil to Asia recently at the expense of the Middle East as Middle East domestic demand fell due to lower power generation requirements over winter, freeing up supplies for Southeast Asia and India West Coast. As a result, Middle East has also ramped up HSFO exports to Asia for the fourth consecutive month due to improved arbitrage economics towards Asia compared to Northwest Europe. The seasonal changes in destinations led to longer voyages to Asia. This phenomenon has led to a build-up in Russian residual fuel oil on water, which has accumulated by 11% month-over-month in January to over 30mb, reaching an 11-month high.

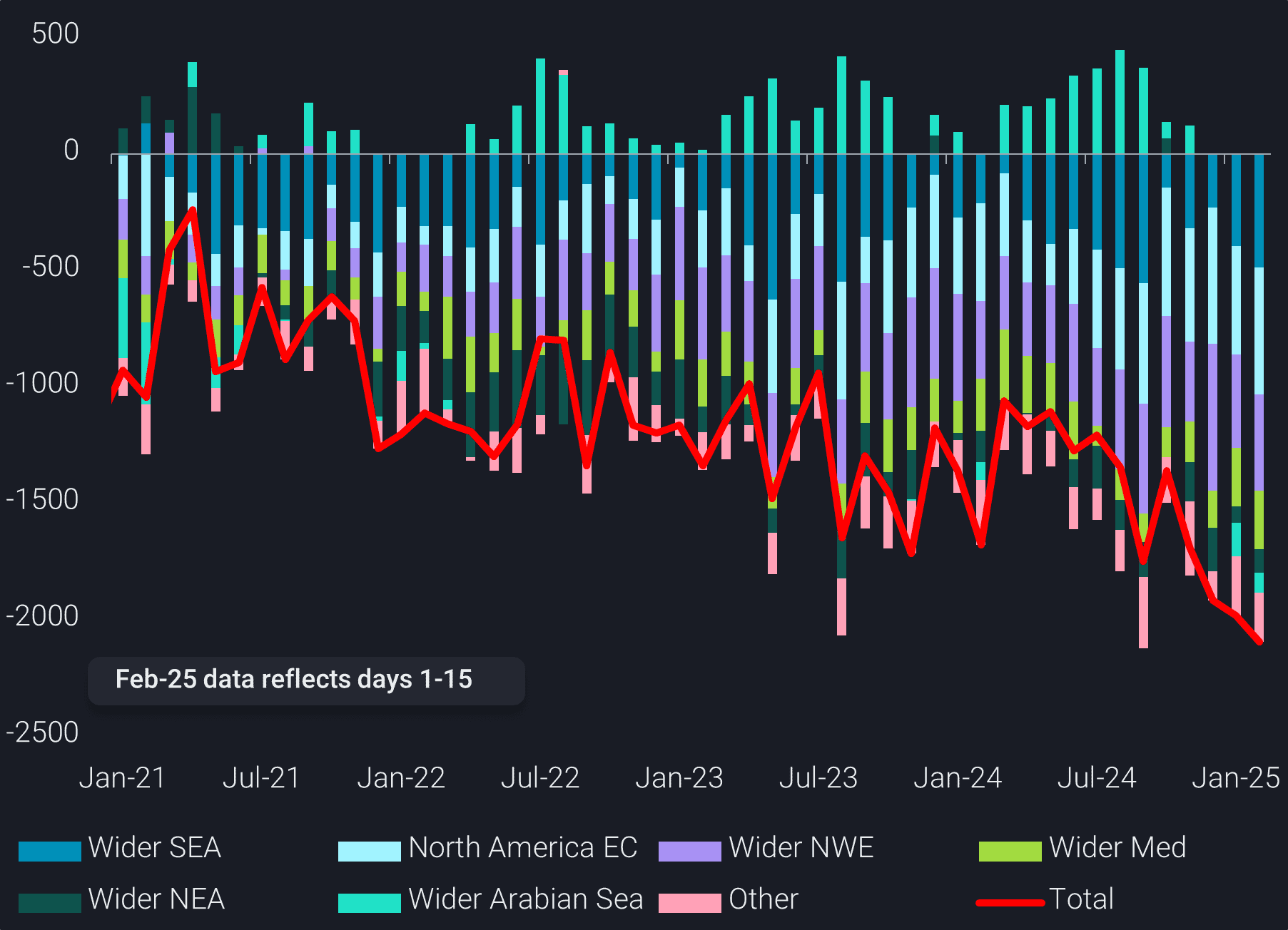

Slowdown in global dirty petroleum product arrivals

There has been a steady reduction of global dirty petroleum product (DPP) arrivals over the past 3 months, reaching a record low of 2.1mbd lost in the first half of February compared to 2016-2019 average levels. The reduction in DPP arrivals over the past 4 years stem from declines concentrated in wider North America East Coast and Northwest Europe. These losses have been somewhat offset by higher arrivals (mostly Russian-origin) into the wider Middle East and West Coast India from 2022 to 2024.

The reduction in global DPP arrivals are a result of newer, more complex refineries coming online over the last two decades, targeting the medium to heavy sour crude slates. Meanwhile over the past five years, many older and less complex refineries with relatively higher fuel oil yields have shut down. This has happened in parallel with a lightening of the global crude slate, driven by increasing United States shale production and lingering OPEC+ production cuts, ensuring DPP supplies will remain pressured.

Global seaborne arrivals of Dirty Petroleum Products by wider shipping region destination (kbd, vs 2016-2019 average)